Insights

All

Blogs

Articles

All

When preparing a business for sale, the Quality of Earnings (QoE) report often becomes a centerpiece of the process. But

When a newly formed SaaS company engaged us 16 months ago, they set a clear goal: to prepare for a

After years of managing diverse revenue streams and expanding its operations, a growing business faced significant challenges in maintaining accurate

As of January 1, 2024, the bipartisan Corporate Transparency Act (CTA) requires many companies operating in the United States to

Valuing a business with precision is critical for a range of strategic decisions, from securing investor funding to executing a

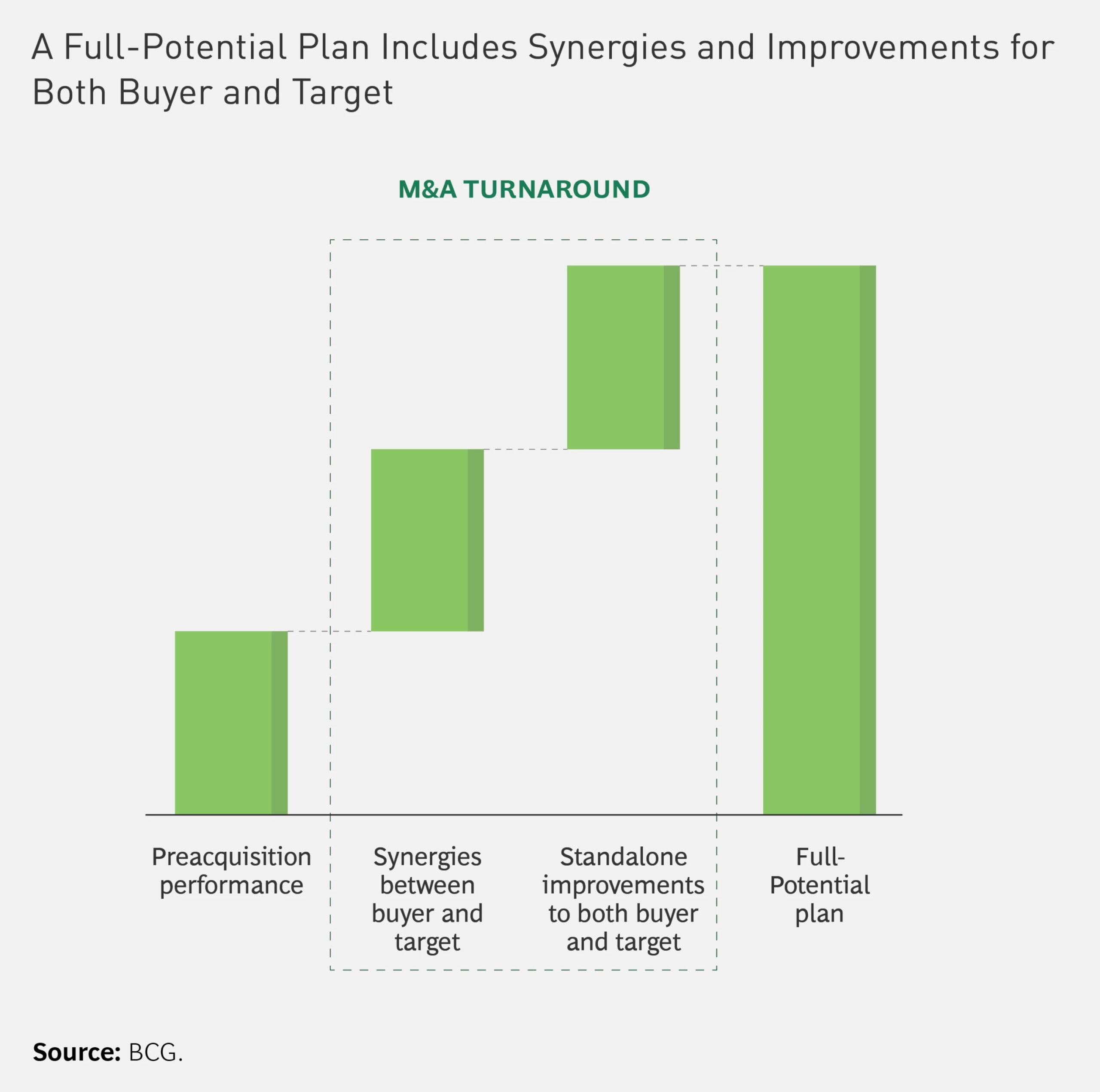

In the evolving landscape of mergers and acquisitions (M&A), the strategic capabilities and vision of the acquiring company profoundly influence

In the dynamic world of business, expansion and diversification are often crucial strategies for long-term success. However, these strategic moves

Discover the intricate world of cross-border stock transactions and unravel the tax implications that multinational companies face.

Taxes are an inevitable part of our financial lives, but savvy investors and entrepreneurs are always on the lookout for

Expanding a business into new markets is a thrilling venture, but it’s also a complex undertaking that requires careful planning

Imagine a global entrepreneur with big dreams setting their sights on the United States, a land of endless possibilities.

In the competitive landscape of fundraising, securing additional capital is a crucial milestone for businesses of all sizes and industries.

Change is the only constant in the world of taxation, and businesses must continually adapt to evolving regulations. One such

Introduction: Greetings to all startup enthusiasts and entrepreneurs! At our accounting firm, we are dedicated to providing valuable insights and

In recent years, interest in environmental, social, and governance (ESG) investing has exploded. This increased interest is a result of

Blogs

When preparing a business for sale, the Quality of Earnings (QoE) report often becomes a centerpiece of the process. But

After years of managing diverse revenue streams and expanding its operations, a growing business faced significant challenges in maintaining accurate

Valuing a business with precision is critical for a range of strategic decisions, from securing investor funding to executing a

In the evolving landscape of mergers and acquisitions (M&A), the strategic capabilities and vision of the acquiring company profoundly influence

In the dynamic world of business, expansion and diversification are often crucial strategies for long-term success. However, these strategic moves

Articles

As of January 1, 2024, the bipartisan Corporate Transparency Act (CTA) requires many companies operating in the United States to

Discover the intricate world of cross-border stock transactions and unravel the tax implications that multinational companies face.

Taxes are an inevitable part of our financial lives, but savvy investors and entrepreneurs are always on the lookout for

Expanding a business into new markets is a thrilling venture, but it’s also a complex undertaking that requires careful planning

Imagine a global entrepreneur with big dreams setting their sights on the United States, a land of endless possibilities.

In the competitive landscape of fundraising, securing additional capital is a crucial milestone for businesses of all sizes and industries.

Change is the only constant in the world of taxation, and businesses must continually adapt to evolving regulations. One such

Introduction: Greetings to all startup enthusiasts and entrepreneurs! At our accounting firm, we are dedicated to providing valuable insights and

In recent years, interest in environmental, social, and governance (ESG) investing has exploded. This increased interest is a result of